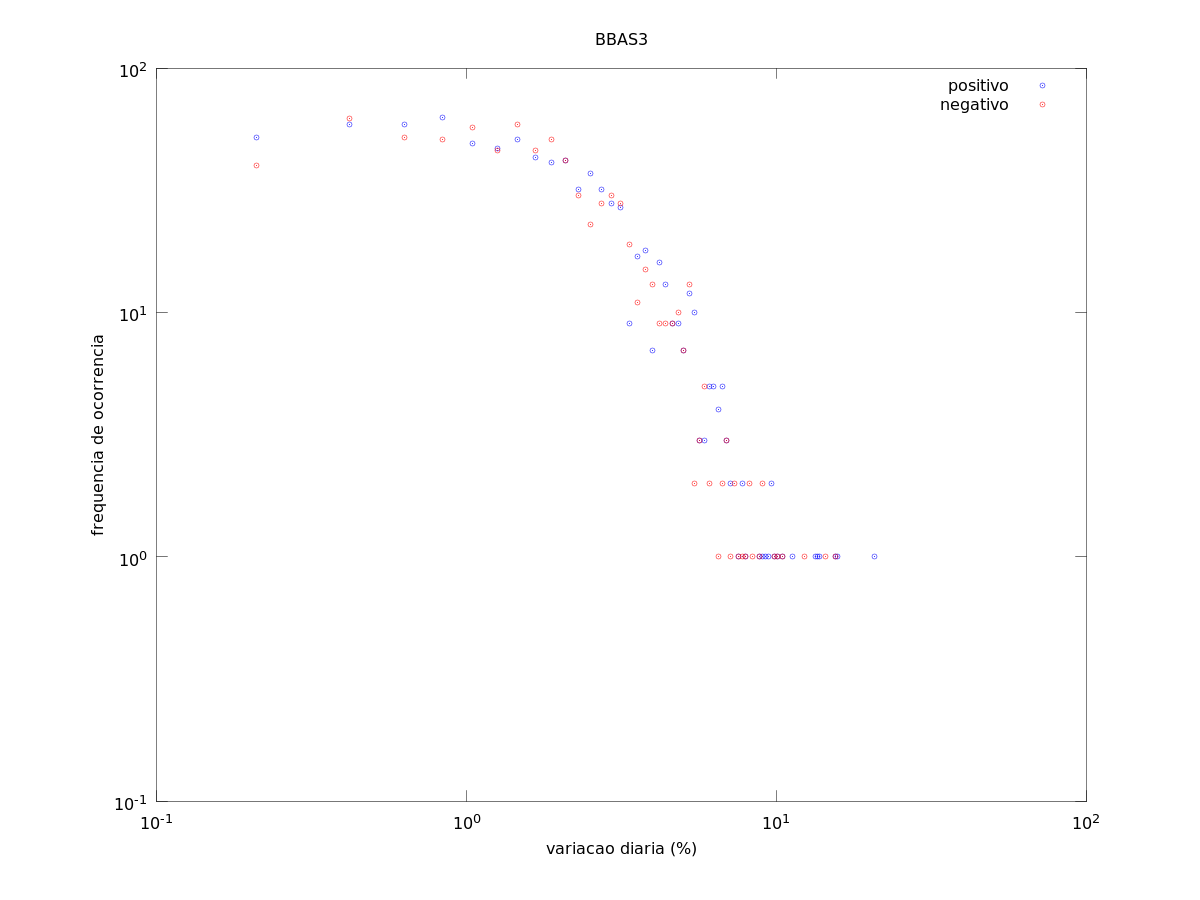

I got some financial assets data and observed the frequency of occurrence of variation within certain ranges. The graphics bellow present this result. In the first graphic, the variation (%) range was linearly sliced. In the second graphic, I made a logarithmic spaced slices. The third image has a linearly spaced slices, but the number of slices is quite smaller.

When the number of slices is smaller, we clearly see a straight line, what means a power law holds. When the number of slices is bigger, it behaves like a line with a saturation for very frequent values.

Petrobras

Bovespa index

Banco do Brasil

"But economics is like sand, not like water. Decisions are discrete, like the grains of sand, not continuous, like the level of water. There is friction in real economics, just like in sand. We don't bother to advertise and take our apples to the market when the expected payoff of exchanging a few apples and oranges is too small. We sell and buy stocks only when some threshold price is reached, and remain passive in between, just as the crust of the earth is stable until the force on some asperity exceeds a threshold. We don't continually adjust our holdings to fluctuations in the market. In computer trading, this threshold dynamics has been explicitly programmed into our decision pattern.

Our decisions are sticky This friction prevents equilibrium from being reached, just like the friction of sand prevents the pile from collapsing to the flat state. This totally changes the nature and magnitude of fluctuations in economics.

Economists close their eyes and throw up their hands when it comes to discussing market fluctuations, since there cannot be any large fluctuations in equilibrium theory: "Explanations for why the stock market goes up or down belong on the funny pages," says Claudia Goldin, an economist at Harvard. If this is so, one might wonder, what do economists explain?

The various economic agents follow their own, seemingly random, idiosyncratic behavior. Despite this randomness, simple statistic patterns do exist in the behavior of markers and prices. Already in the 1960s, a few years before his observations of fractal patterns in nature, Benoit Mandelbrot analyzed data for fluctuations of the prices of cotton and steel stocks and other commodities. Mandelbrot plotted a histogram of the monthly variation of cotton prices. He counted how many months the variation would be 0.1% (or

-0.1% ), how many months it would be 1%, how many months it would be 10%, etc. He found a "Levy distribution" for the price fluctuations. The important feature of the Levy distribution is that it has a power law tail for large events, just like the Gutenberg-Richter law for earthquakes. His findings have been largely ignored by economists, probably because they don't have the faintest clue as to what is going on.

Traditionally, economists would disregard the large fluctuations, treating them as "atypical" and thus not belonging in a general theory of economics. Each event received its own historical account and was then removed from the data set. One crash would be assigned to the introduction of program trading, another to excessive borrowing of money to buy stock. Also, they would "detrend" or "cull" the data, removing some long-term increase or decrease in the market. Eventually they would end up with a sample showing only small

fluctuations, but also totally devoid of interest. The large fluctuations were surgically removed from the sample, which amounts to throwing the baby outwith the bathwater. However, the fact that the Iarge events follow the same behavior as the small events indicates that one common mechanism works for all scales -- just as for earthquakes and biology.

How should a generic model of an economy look? Maybe very much like the punctuated equilibrium model for biological evolution described in Chapter 8. A number of agents (consumers, producers, governments, thieves, and economists, among others) interact with each other. Each agent has a limited ser of options available. He exploits his options in an attempt to increase his happiness (or "utility function" as the economists call it to sound more scientific), just as biological species improve their fitness by mutating. This affects other agents in the economy who now adjust their behavior to the new situation. The weakest agents in the economy are weeded out and replaced with other agents. or they modify their strategy, for instance by copying more successful agents.

This general picture has not been developed yet. However, we have constructed a simplified toy model that offers a glimpse of how a truly interactive, holistic theory of economics might work."

(How Nature Works: The Science of Self-Organized Criticality, Per Bak)

Leo,

ResponderExcluirAnalisei um a um os gráficos. Eles me lembram bastante o caso de sinais que têm distribuição uniforme para pequenas variações e um decaimento cuja inclinação aumenta à medida que as variações aumentam.

Hani